For over a decade, every mobile studio paid the same rent: 30% to Apple or Google, no negotiation, no alternative. Gil Tov-ly has watched the entire ecosystem bend against that reality — and now, as CMO of Appcharge, he's helping studios take it back.

When mobile gaming was young, the platform tax felt like a fair trade. Apple and Google handled payments, taxes, chargebacks, and compliance. Developers got distribution. The 30% fee was the price of admission to a system that worked — until it didn't.

"Building a hit game is hard," Gil told us on the Player Driven podcast. "And then scaling that into a big business for five thousand people, doing it in a cost-efficient, positive-margin way — that's really hard, especially ever since iOS 14 and ATT. Any piece of margin you can scrape goes a long way."

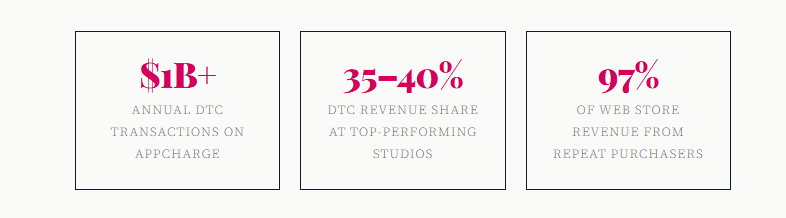

Gil has lived the entire arc. From AdTech and user acquisition in Tel Aviv's early mobile ecosystem, through a cloud gaming startup and five years building Overwolf's UGC platform to 100 million gamers, to his current role as CMO at Appcharge — where the company recently crossed $1 billion in annual DTC transactions. That number isn't an experiment. It's proof that the direct-to-consumer model has arrived.

Why the 30% Model Finally Started Cracking

Two structural forces broke the status quo, and Gil saw both in real time.

The first was Apple's App Tracking Transparency framework in iOS 14. Before ATT, user acquisition ran on precise targeting using device identifiers — a profitable, reliable machine. When Apple required user opt-in for tracking, that machine broke. Acquisition costs spiked. Studios that had been breakeven started bleeding. The 30% platform fee suddenly felt unconscionable when the rest of the economics had deteriorated.

The second force was Epic Games. Tim Sweeney's legal battles against Apple and Google — waged across multiple jurisdictions — pulled regulators into a conversation that developers had been afraid to have publicly. Were these restrictions on alternative payments unfair? Were studios being locked out of their own business relationships with their own players?

"Epic really ushered in this age of DTC," Gil explained. "After years of legal battles, we're now seeing studios reach 35 to 40% of their revenue from DTC — and they're taking back control of their margins, their profitability, their destiny."

What a Web Store Actually Is (and What It Isn't)

Gil's elevator pitch for Appcharge: "Shopify for mobile games." A web store is a branded website where players can purchase the same items available in-game — gems, coins, battle passes, cosmetics — and have them delivered directly to their account. Same inventory, different checkout, dramatically different economics.

The fee differential is significant. Where Apple and Google charge up to 30%, Appcharge typically charges studios between 4% and 5% of transaction volume. For a studio routing 35–40% of revenue through DTC, that margin recovery funds additional user acquisition, headcount, and product investment.

But the infrastructure challenge is real. When Gil joined Appcharge two years ago, he found a company that had been operating for just 18 months — and already had ten legal entities, SOC 2 certification, PCI compliance, and a full fintech stack. "I was amazed," he said. "How did you build this in a year and a half?" Tax compliance across 5,000+ US tax jurisdictions, chargeback handling, global payment rails — this is the moat that makes DTC hard to replicate in-house.

The Trust Problem (And How It Gets Solved)

Player skepticism of web stores was — and still is — a genuine barrier. Sending a player outside an app to a browser checkout feels unfamiliar. Gil is direct about the design philosophy Appcharge brings to this problem.

"When we build a store, we always use the official game domain, never ours," he said. "The store looks and feels like the game — the animations, the button radius, the color palette, the font. And the login flow is that you pass through the game app. One click, through the app, and you're authenticated."

An interesting data point from Appcharge's transaction reports: PayPal is dramatically overrepresented in web store payments compared to standard e-commerce. In some markets — Germany being a notable example — PayPal accounts for a startling share of web store purchases. Gil's interpretation: players choose PayPal specifically because they trust its buyer protection when navigating an unfamiliar checkout for the first time. The payment method choice is itself a trust signal.

And once players do convert? The retention is strong. "97% of the revenue on web stores comes from repeat purchasers," Gil noted. "Establishing that habit is everything."

Payment Links: DTC Enters the Game Session Itself

The more technically interesting development is what Appcharge calls "payment links" — a feature that brings the DTC choice point into an active game session. A player encounters an in-app purchase moment and sees two options: buy 1,000 coins in-app for $10, or buy 1,200 coins on the web for the same price. The extra value is the incentive to accept the extra friction.

The concern studios had: will sending a player to a browser kill the impulse purchase moment? Will they come back? Appcharge's data answered both questions. Conversion rates on the payment link flow reached up to 92%. And critically — there was zero measurable cannibalization. Players complete the web purchase and return to the game. In-app and web store revenues grow together, not at each other's expense.

Some studios now drive 50% of their DTC revenue through payment links alone.

The New Org Structure: The Rise of the DTC Role

The institutional adoption of DTC is visible in studio org charts. Gil pointed to Scopely having a VP of DTC — a dedicated executive-level role overseeing the entire direct commerce function across the company's portfolio. This is the normalization signal: when a function gets a VP, it's no longer a side project.

The internal dynamics are real but manageable. A game GM optimizing their P&L may have different preferences than a centralized publisher team making platform decisions for multiple titles. The CTO evaluates integration overhead. The CFO either becomes the biggest champion — seeing the margin impact directly — or the final gate. Gil's approach: understand which function leads at each client, and meet them there.

Who Cracked DTC First — and Who's Coming Next

The social casino genre pioneered the model because its economics made the math obvious. Social casino games already had VIP account management — direct relationships with high-spending players. Converting a thousand top spenders to a web store could shift 30% of total revenue to DTC almost immediately. Studios like Playtika wrote the original DTC playbook.

What's changed is the democratization. Casual games — which operate at a different scale and with a different player spending profile — are now reaching DTC revenue shares that would have seemed implausible a few years ago. "Some of our clients like CandyVore are able to transition tens of thousands, even hundreds of thousands of players to the web store consistently," Gil said. "It's not just for the social casino segment anymore."

Where DTC Goes in 2026

Gil sees two dominant trends defining the next phase.

First: DTC goes deeper into the native app experience. Regulation — particularly in the EU and US markets impacted by the Epic v. Apple rulings — is forcing platforms to decouple their service fees from their payment processing fees. That means third-party payment providers like Appcharge can now integrate inside the official in-app experience. "Imagine purchasing through Appcharge inside the app, from the regular in-game store, not through Google — and the experience is seamless." That's the direction.

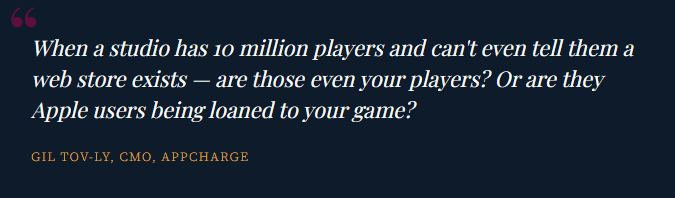

Second: the real unlocked asset isn't the margin — it's the player relationship. When everything ran through Apple and Google, studios didn't own their player data. They didn't have emails, payment credentials, or direct communication rights. "Those are Apple users being loaned to your game," as Gil put it. DTC forced studios to build direct relationships: email lists, Discord communities, WhatsApp groups, CRM infrastructure.

"If you look at the typical big game now, it's no longer just having a TikTok account," Gil observed. "These teams operate sophisticated communication channels, Discord groups, community management, town halls where players learn about new lore and new campaigns. We're going to see more investment in that in 2026 because studios have realized how critical it is to their future."

Key Takeaways

The 30% platform fee is no longer the only path — Appcharge's 4–5% model is proven at $1B+ in transactions

Top studios are now routing 35–40% of revenue through DTC, with that margin funding growth

Trust, not friction, is the real barrier to web store adoption — and it's solvable through design

Payment links bring the DTC choice point into the game session with no measurable cannibalization

Social casino wrote the playbook; casual and strategy are now following

Regulation is opening the door for in-app third-party payments — a significant next frontier

The player relationship is the asset — DTC forces studios to finally own it

The Bigger Shift

Gil frames the DTC movement not as a monetization trick but as a structural rebalancing of power in the games industry. For over a decade, studios built products on top of platforms they didn't control, for players they didn't own, paying a tax on every dollar. The legal, regulatory, and economic conditions that made that arrangement stable have all shifted simultaneously.

The studios that started early are now seeing the compounding effects: better margins funding more UA, better UA funding more players, more players supporting the community infrastructure that makes games last longer. "After so many years of mobile gaming struggling — waves of layoffs, compressed margins — I'm so optimistic about what I'm seeing," Gil said. "It's exciting to be in mobile gaming again."

That optimism is backed by a billion dollars of evidence.